Neobank wallet (the modern baseline)

Who uses it: Fintech team building a digital-only bank

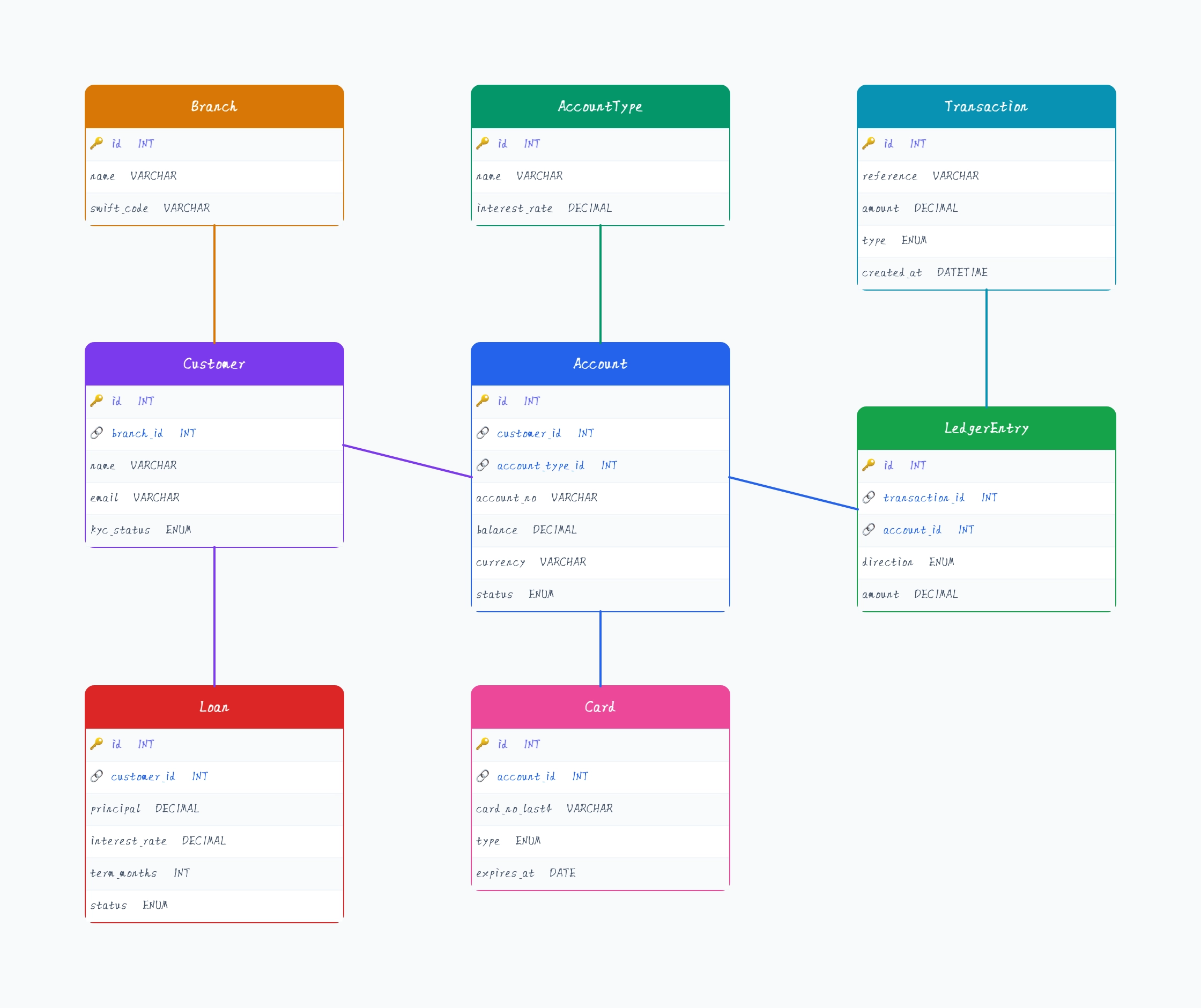

Customer with kyc_status and document references

Account simplified — usually one wallet per customer

Transaction always produces two LedgerEntry rows

Card issued from a card-network partner (Visa/Mastercard)

No physical Branch — replace with an Issuer reference

Why this works: Neobanks strip the schema to its essentials — one wallet per customer and a clean double-entry ledger. The diagram drops branches in favor of a partner reference, since the customer never visits one.